Contactless payments (in their various forms) are currently the fastest method of electronic payment. By tapping or waving a contactless card, smartphone, or wearable device over a payment terminal, which – as if by magic – accepts the transaction. But it’s not magic. So, how do they work? Let’s break it down.

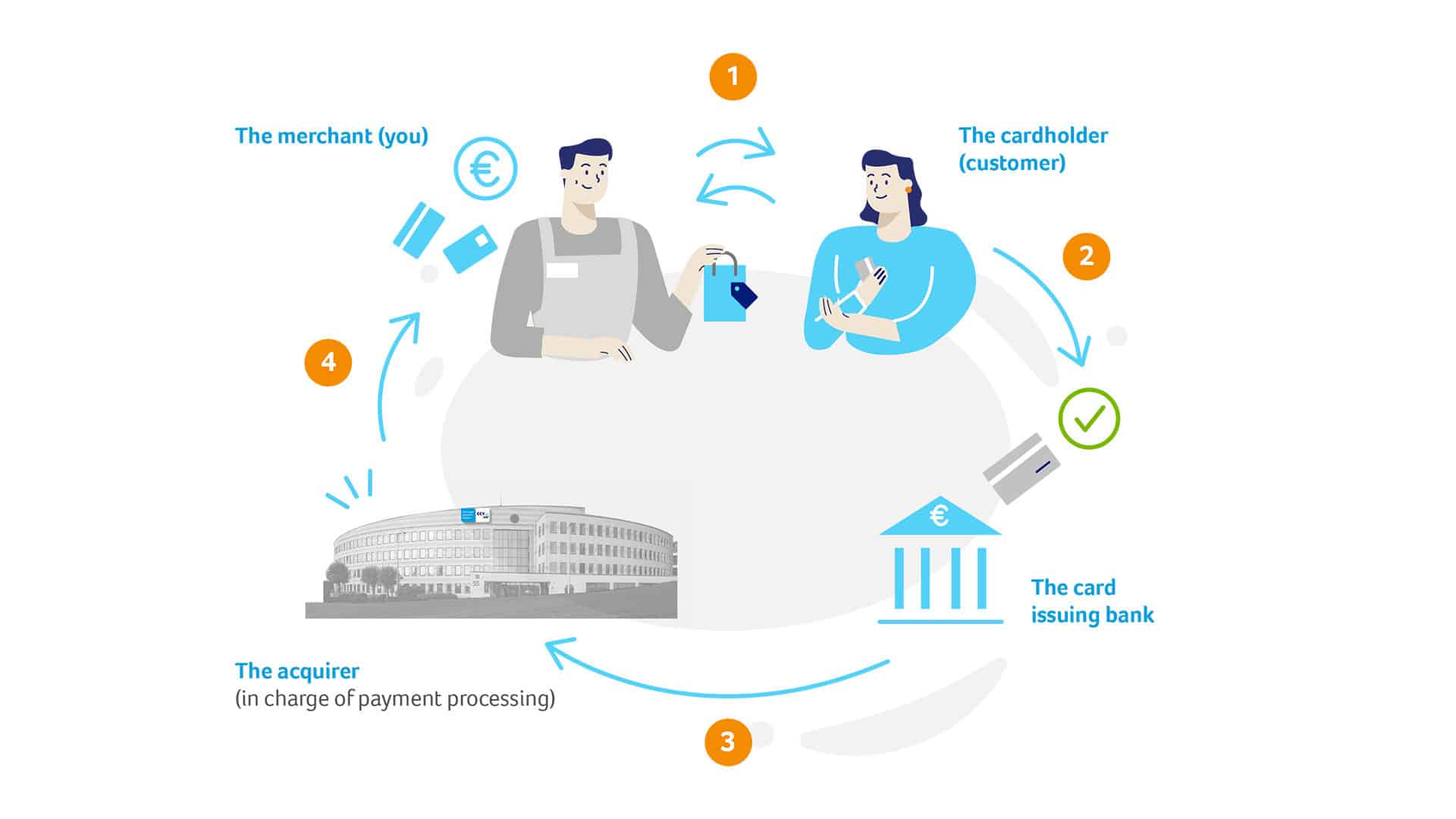

- The merchant sets the total purchase amount on the terminal and the customer presents their card.

- The card information is sent to the card-issuing bank. If the information is valid, payment is approved and the second part of the process begins.

- Next, the money is transferred in the opposite direction, from the bank, through the acquirer, and to the merchant’s bank account.

- When the merchant receives payment, the process is complete.

A contactless debit or credit card has a built-in microchip which is capable of emitting radio

waves. The card also has an antenna in the plastic designed to secure the connection with a card

reader. The technology at play here is called near field communication, or NFC for short. To pay for something, the customer holds their contactless card near to the reader, allowing the card’s microchip and the card reader to communicate with one another. The card reader sends the transaction details, the card sends back the payment details, and the merchant’s payment processor handles the payment  Smartphones, smartwatches, and other wearable devices capable of contactless payment also use near-field communication (NFC) to send and receive transaction data.

Smartphones, smartwatches, and other wearable devices capable of contactless payment also use near-field communication (NFC) to send and receive transaction data.

Once the NFC chip is held within close proximity of a reader, it begins a wireless data transfer. These devices usually require biometric authentication (such as fingerprint scan or facial recognition) to authorise the payment – but also an on-screen PIN can be requested for security.

Although not as popular as cards or NFC-equipped devices, QR (quick response) codes are still a viable option for accepting contactless payments. QR codes store hundreds of times more information than traditional vertical barcodes and can be scanned both from screens and printouts.

Most smartphones using the latest software can scan QR codes from directly within the main camera app, meaning there’s no need for third-party apps. Your customer would simply open the camera, point it at the code, and follow the instructions on their device to complete the transaction.